The shift towards collaborative contracting models in public works is gaining momentum in Singapore, underscored by the recent award by Jurong Town Council (JTC) to Eng Lam Contractors Co (Pte) Ltd for infrastructure works at CleanTech Loop (Phase 2A) using NEC4 Option C: Target Cost Contract1. While conceptually promoting shared risk and reward, Option C is renowned for its administrative demands and introduces commercial exposures that contractors must manage diligently.

Contractors engaging in this model must look beyond the collaborative theory to understand the practical realities of execution, which revolve heavily around the meticulous management of cost, time, and documentation.

The Target Cost Mechanism: Theory vs. Reality

NEC4 Option C operates on a pain/gain share principle relative to an agreed Target Price (the sum of the initial Prices and subsequent Compensation Event adjustments)2

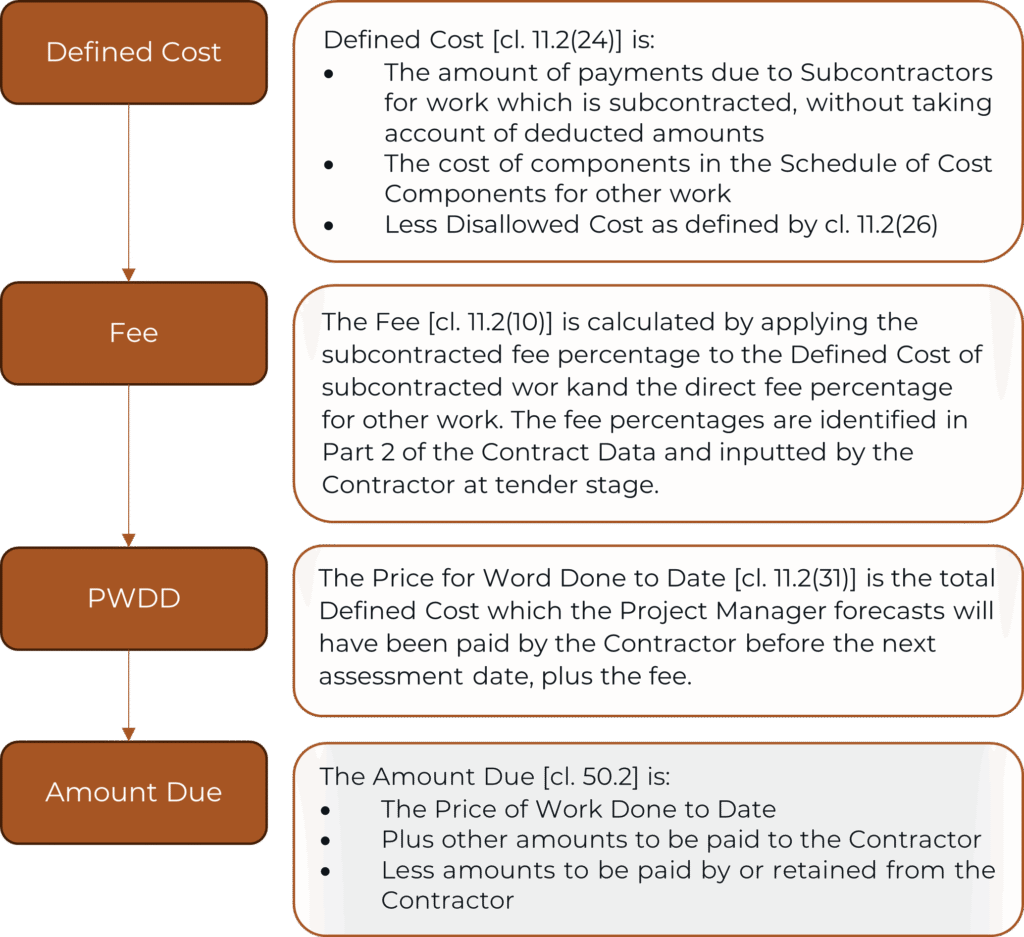

- The Price for Work Done to Date (PWDD): This is the running reimbursement for the contractor, calculated as Defined Cost (actual costs incurred as per the contract’s Schedule of Cost Components) plus the Fee.2

- The Pain/Gain Share: The final PWDD is compared to the final Target Price. An underspend (PWDD < Target Price) results in a gain shared by both parties, while an overspend (PWDD > Target Price) results in pain that is also shared according to pre-agreed percentages.3

In practice, the success of this mechanism hinges on the strict control of Defined Cost and the rigorous avoidance of Disallowed Costs, which are borne entirely by the Contractor, irrespective of the pain/gain share.4 The process of assessing the amount due is illustrated as follows:

Critical Watch-Outs for Contractors in NEC4 Option C

The administrative intensity and cost-reimbursable nature of Option C introduce specific commercial pitfalls that contractors must navigate:

1. The Financial Exposure of “Disallowed Costs”

The most significant financial risk is the Project Manager deeming incurred costs to be “Disallowed Costs” (Clause 11.2(26)).4 These are non-recoverable and represent an absolute loss to the contractor. Common triggers include:

- Failure of Records: Costs are disallowed if they are “not justified by the Contractor’s accounts and records”.4 This demands an open-book, auditable cost-capture system from day one.

- Failure to Give Early Warning: Costs incurred “only because the Contractor did not… give an early warning” are disallowed.4 The NEC4 principle of proactive notification (Clause 16.1) must be strictly followed to protect financial entitlement.5

- Defects and Unused Resources: The cost of “correcting Defects after Completion” is disallowed. Similarly, the cost of Plant and Materials or resources “not used to Provide the Works” (after allowing for reasonable wastage/utilisation) is disallowed, requiring careful site management and procurement control.4

2. Target Price Integrity and Compensation Events (CEs)

The Target Price must remain a realistic benchmark. Contractors must ensure CEs are valued and agreed upon promptly. A delay in assessing CEs means the Target Price remains artificially low, creating an illusion of overspend that may trigger an interim deduction under the pain share or put undue pressure on the contractor.3

3. Subcontractor Alignment

The Main Contractor’s commercial exposure is directly affected by their supply chain. It is critical to ensure that subcontractor agreements (ideally using NEC4 subcontracts) include provisions for:

- Strict adherence to the Defined Cost components.

- Flow-down of Disallowed Cost triggers, especially those related to record-keeping and early warnings.

- Notification to the Project Manager of any disputes with subcontractors to prevent dispute costs from becoming Disallowed Costs against the Main Contractor.6

Comprehensive Commercial and Contractual Support

Successful execution of NEC4 Option C requires specialist expertise spanning the entire project lifecycle to mitigate the risk of pain and maximise gain.

|

Project Stage |

Focus Area |

Essential Support Action |

|---|---|---|

|

I. Pre-Contract |

Risk Allocation and Target Setup |

Detailed review of bespoke Z-Clauses and the definition of Disallowed Costs.4 Strategic negotiation of the pain/gain share percentages and realistic Target Price assumptions.3 |

|

II. Project Execution |

Cost Management and Compliance |

Implementation of a compliant Cost Capture System (PWDD) to ensure all Defined Costs are auditable and verifiable.2 Proactive management and submission of Early Warning Notifications (EWN) and Compensation Events (CE) (Clause 61.1) to protect the Target Price.5 |

|

III. Project Closeout |

Account Finalisation and Audit |

Independent assessment and verification of the final PWDD against the Target Price. Expert support in defending against any Project Manager’s certification of Disallowed Costs and validating the final pain/gain share calculation.4 |

By embedding proactive commercial management, contractors can transform the administrative burden of Option C into a mechanism that truly delivers on its promise of shared success.

Footnotes:

- JTC awarded the infrastructure works contract at CleanTech Loop (Phase 2A) to Eng Lam Contractors Co (Pte) Ltd using NEC4 Option C, marking the first NEC4 adoption in the Singapore public sector.

- NEC4 Option C defines the Price for Work Done to Date (PWDD) as Defined Cost plus Fee, and payment is based on this actual, auditable cost.

- The pain/gain share mechanism compares the final PWDD to the Target Price, with overspend or underspend shared between the Client and Contractor as agreed in the Contract Data.

- NEC4 ECC Clause 11.2(26) defines Disallowed Cost, which are non-recoverable by the Contractor and include costs not justified by records, costs due to failure to give an early warning, and costs of correcting Defects after Completion.

- Failure to provide an Early Warning that the Contractor is required to give can lead to the additional costs incurred being disallowed, reinforcing the administrative necessity of Clause 16.1.

- NEC4 requires the Contractor to notify the Project Manager of preparations for adjudication or tribunal proceedings with a Subcontractor or supplier to avoid such costs being disallowed between the Parties.

Contact Us

Mr. Leslie Harland is a Chartered Quantity Surveyor and internationally recognised construction quantum expert, with more than three decades of experience in the construction and engineering industry. He has advised clients on a wide range of construction and engineering matters, including liability for disputed variations, complex final account negotiations, unforeseen ground conditions, defective works, variation pricing, and claims for acceleration, disruption, and extensions of time. Leslie has provided oral testimony (in person and by video link) in multiple jurisdictions, including Singapore, the United Kingdom, the United States, South Africa, Dubai, and South Korea.

Contact Leslie to learn more about the services Rimkus Quantum Experts can provide.

Leslie Harland, MSc, MRICS, MCIOB, MCInstCES, ACIArb

Director, Quantum Expert

+65 9272 6295

[email protected]